You can’t fix a slump – stay with it – because feeling a tad disillusioned by your investment portfolio is a sign of the times. For the best part of five years, investors could be excused for thinking they’ve been hitting the replay button on a bad repeat of bleak market conditions. While global markets have rallied, especially in the US, South African investors have sadly missed out. “Stay the course, ride the storm and don’t feel tempted to make changes for the sake of trying to fix things,” advises Eugene Visagie of Morningstar Investment Management SA (MIMSA). After prolonged periods of low returns, we often find ourselves being tempted to ‘do something’, to make a change and to fix what’s not working. However, this can be precisely how wealth is destroyed over time.

Nobody wants to get rich slowly

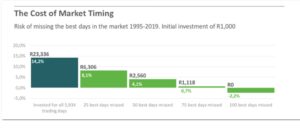

Equities deliver real returns to patient investors. “While nobody wants to get rich slowly, the irony is that it pays to stay the course,” says Visagie. If an investor had been exposed to the South African equity market from 1 January 1995 to 30 April 2019, they would have generated an annual return of 14.2%. This period includes tough market conditions, including the emerging market crisis in 1998, the tech bubble of the early 2000s and the global financial crisis in 2008/09 – plus the last five years during which the local equity market has been relatively flat. After inflation is accounted for, this is an annualised real return of just over 8% per annum in 23 years. “The numbers are clear; don’t worry about the noise, think long-term,” advises Visagie. In spite of the evidence, the temptation exists to attempt to time the market – that is, pick an entry and/or exit points. “We believe that trying to time the market is a fruitless exercise,” says Visagie. “Often, the best time to invest is when things feel most uncomfortable.” If you had tried to time the market over the past 23 years and missed just the best 100 days of the total 5,934 trading days, your return would have been -2.2% per annum, instead of 14.2% per annum for the full period.

It’s clear, staying the course works. Yet, despite the compelling evidence, there has been a material move by investors out of equities and into more conservative money market and fixed income products. Indeed, these asset classes provide a comfortable return profile with more predictable returns, and they have rewarded investors with positive returns over the past few years. Has this been an appropriate course of action? Time will tell, of course, but Morningstar wouldn’t rule out a comeback for the unit trust industry, especially given that the largest casualty has been the multi asset/balanced funds which used to take the lion’s share of industry flows. “Despite disappointing performance from local risk assets and balanced funds in the recent past, we believe that investors with a medium- to long-term horizon need exposure to these assets to generate inflation-beating returns,” says Visagie. He explains that investors run the risk of not achieving their financial goals if they move between different asset classes based on short-term performance.

Looking forward – the bigger picture

As we enter the mid-year mark in 2019, perhaps the core message is that beaten-up assets can do surprisingly well going forward. Many forget the important role that starting valuations play when judging the ability of assets to generate above-average future returns. So, where does that leave us? “In the short term, it’s anyone’s guess – we’ve never claimed to have a crystal ball- , although we can see some interesting opportunities presenting themselves when looking purely at valuations,” says Visagie.

Value. The economy is not the market. What matters most is to not overpay for a stream of long-term cash flows. Many domestically-focused businesses remain out of favour due to the persistent gloomy economic outlook in South Africa. With the possibility of policy reform geared towards the goal of economic growth, investment managers are aware (albeit with caution) of any unlock that could potentially materialise from purchasing these assets below fair value.

Risk. Risk is the permanent loss of capital. In buoyant market conditions, don’t be distracted by any euphoric claims or the general feeling of calm. Morningstar’s process is aimed at unlocking value from unloved areas by focusing on what we can control – incorporating a disciplined long-term valuation-driven approach.

Diversification. Visagie advises that, “While value exists in certain areas of our market, we are conscious of staying true to our disciplined investment process, thereby minimising the ill-effects that behavioural biases can have on investor outcomes. Our asset allocation framework provides a tried and tested method for building portfolios that is not reliant on one market outcome. Our view is that a diversified portfolio tilted towards asset classes with higher future expected returns, within appropriate risk constraints, provides the best chance of delivering outcomes in line with our investors’ objectives.”

There’s no doubt that the current market conditions are unsettling for some. It is at these moments that we would discourage investors from making changes that could harm their ability to reach their financial goals. It is often during these difficult times that we have the greatest opportunity to add value for our clients, acting rationally when others struggle to do so.

Morningstar Investment Management South Africa | 10 June 2019